Legal help that’s

free for you.

Just a phone call away.

What do you have to lose?

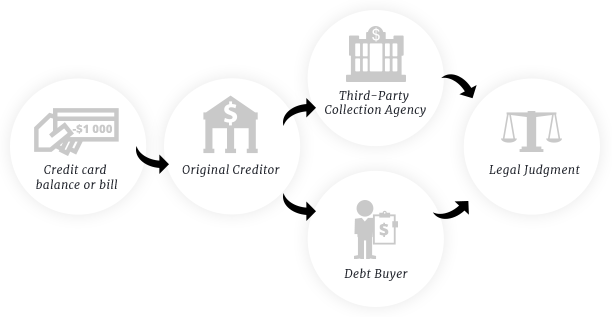

A debt can take on a life of its own. Here’s an example: An old credit card balance sits on the creditor’s books for awhile, and you receive calls or letters from the creditor asking for payment. The creditor might use an automated dialer to robocall your cell phone. When you answer the phone, you may hear a prerecorded voice, or a series of clicks before you’re connected to a live person.

If you didn’t give your permission for the creditor to robocall your cell phone, it’s a violation of the Telephone Consumer Protection Act.

But let’s say you aren’t able to pay the creditor. Next, it heads in one of two directions: either the debt is forwarded on to a third-party collection agency, which collects on behalf of the creditor, or it’s bundled in with other unpaid debts and sold to a debt buyer. Both the third-party collector and the debt buyer are required to follow the Fair Debt Collection Practices Act (FDCPA). All too often, though, debt collectors and debt buyers engage in coercive, threatening, or harassing behavior that’s illegal.

Once you tell the debt collector that Lemberg Law represents you,

the calls and letters must stop.

When you call Lemberg Law, we get to the heart of the matter. We ask questions. We listen carefully. We dig a little deeper. We answer every question you have and those that might crop up later. We give you our honest assessment about the prospects for your case and what you might be able to recover.

If you’re dealing with a third-party collection agency, once you tell the debt collector that Lemberg Law represents you, the calls and letters must stop. From that point on, all calls and letters from the debt collection agency must come to us.

In both FDCPA and TCPA cases, we typically start by contacting the creditor or collection agency. They’ll review their records. If they know that they violated the law, they may offer to settle the case before a complaint is ever filed in court. If they dispute the violation, we go ahead and file a complaint in federal court and demand a jury trial.

Often, the creditor or agency offers to settle after the discovery process, when it’s evident that the law was violated. If a settlement is offered, we’ll provide you with all the information you need in order to make the decision that works best for you. If you decline the settlement or no settlement is offered, we proceed with the court case. We’ll doggedly fight for your rights and consult with you every step of the way.

In FDCPA cases, the agency violating the law is responsible for paying your legal fees and court costs. In TCPA cases, we work on contingency, and don’t get paid unless you win. Either way, you never have to pay a dime out of pocket.

Legal help that’s

free for you.

Just a phone call away.

What do you have to lose?

Lemberg Law is dedicated to making collectors pay when they violate the Fair Debt Collection Practices Act or the Telephone Consumer Protection Act.

The firm’s main office is located at 43 Danbury Road, Wilton, Connecticut.